AML Transaction Monitoring in The UAE: Regulations & Best Practices

Accelerate AML Compliance: Meet Regulatory Demands with 80% Less Setup Time

The UAE plays a key role in global finance, sitting right where Asia, Europe, and Africa meet. Its economy is varied, with free trade zones and business-friendly rules bringing in a lot of foreign investment and international deals. This special spot on the map offers big opportunities but also creates challenges, like fighting money laundering and illegal financial activities.

While the UAE’s strong economic setup drives growth, its open financial system can be misused. Free trade zones, meant to make business easier, sometimes allow activities like trade-based money laundering. The complexity of modern financial systems, coupled with geopolitical dynamics, makes AML transaction monitoring a critical tool for maintaining financial integrity.

AML Transaction Monitoring in the UAE

AML, or Anti-Money Laundering transaction monitoring, is a systematic process that checks and reviews financial activities to spot and stop illegal actions like money laundering and fraud. Modern transaction monitoring tools look at customers’ actions, patterns in transactions, and outside factors to find anything unusual that needs a closer look.

AML transaction monitoring in the UAE helps the country meet global standards like FATF guidelines and maintain its image as a trusted and secure place for business.

The Importance of AML Transaction Monitoring in the UAE

The UAE is a big player in global trade and finance, pulling in businesses and investors from all corners of the world. This open setup is great for growth, but it can also make it easier for criminals to misuse the system. That’s where AML transaction monitoring in the UAE comes in. Let’s break the importance of transaction monitoring processes down:

1. Protecting the UAE’s Reputation

The UAE’s success depends a lot on trust. A solid system for the transaction monitoring process to catch and stop financial crimes shows the world that the UAE takes its responsibilities seriously and keeps investors confident and makes businesses feel safe working here.

If UAE got a reputation for money laundering, businesses and investors might start to worry which could in turn, lead to a drop in foreign investment and fewer international partnership

2. Helping Honest Businesses Thrive

When you can quickly spot and handle suspicious transactions, it means fewer delays and headaches for everyone else. Honest companies get to focus on what they do best without being dragged down by criminal activity around them.

3. Reducing Risk

The UAE handles a ton of international money and trade, especially in its free trade zones, and these zones make business easier, but they can also be a magnet for money laundering. Therefore, smart transaction monitoring tools like FOCAL transaction monitoring tools enable the UAE to catch these issues early and stop them before they cause any harm.

4. Avoiding International Sanctions and Penalties

If a country became widely known for money laundering, global organizations like the Financial Action Task Force (FATF) and countries with strict financial regulations might take action against that country.

This could mean penalties, restrictions on international banking, or being added to Grey lists or even blacklists. Such measures would make it harder and more expensive for businesses in the UAE to trade internationally.

Comply quickly with local/global regulations with 80% less setup time

How the UAE Regulates Financial Monitoring

The UAE has clear and strict rules to catch and stop money laundering!

1. Main Laws

- Federal Decree-Law No. (20) of 2018: sets out the general framework for AML and CFT activities, specifying penalties for non-compliance and giving authorities the power to seize suspicious funds.

- Cabinet Decision No. (10) of 2019: This decision focuses on the obligations of financial institutions, ensuring they adopt effective transaction monitoring systems, and requires them to report suspicious activities through the goAML platform.

Along with these, there are other important decisions that add more detail and help make the rules work better:

- Cabinet Decision No. (58) of 2020: This decision adds further details on the procedures financial institutions must follow to stay compliant with the AML/CFT regulations.

- Cabinet Resolution No. (53) of 2021: This resolution outlines guidelines for non-financial businesses and professionals (DNFBPs), such as real estate agents and lawyers

- Cabinet Decision No. (16) of 2021: This decision provides clarifications on the implementation of financial transaction monitoring UAE and reporting by various entities, especially in the context of high-risk activities.

- Cabinet Resolution No. (74) of 2020: This resolution focuses on the roles and responsibilities of the UAE's Financial Intelligence Unit (FIU).

2. Main Regulators

- Central Bank of UAE

- Ministry of Economy

- Virtual Asset Regulatory Authority (VARA)

3. Penalties for Non-Compliance

If an entity doesn’t follow the laws meant to stop money laundering, it can face serious consequences, so depending on the situation, it could be hit with fines as high as AED 5 million, sent to prison, or even have its business license taken away. The penalty really depends on how serious the violation is.

AML Transaction Monitoring Systems

There are various aspects to understand about AML transaction monitoring systems in the UAE.

1. How AML Transaction Monitoring Systems Work

AML transaction monitoring systems find and track suspicious financial activity. They aim to spot unusual transaction patterns that could indicate illegal activities, minimize unnecessary alerts to keep operations smooth and efficient and ensure that businesses stay compliant with the relevant regulations.

- Gathering Information

First, these systems collect information about all transactions, customer details, and even external data like the country where the transaction happens. All this is put together in one place so it can be looked at easily.

- Spotting Unusual Patterns

Next, the transaction monitoring system looks for warning signs, such as:

- Large transactions that don’t match a person’s usual activity.

- Transfers of money between countries that seem unusual.

- Frequent small transactions that stay just below a set limit.

- Sudden spikes in account activity inconsistent with the customer profile.

- Multiple accounts funneling funds into a single account.

- Transactions with no apparent business purpose.

- Risk Scoring and Alerts

After looking at all the gathered information, the system gives each transaction a risk score. If something seems suspicious, it sends an alert to the team that checks into it. The risk might be higher if the customer is a Politically Exposed Person (PEP) or if there are certain countries (like high-risk countries) involved.

- Checking and Reporting

When an alert pops up, the compliance team looks into it. They might ask Is their identity clear? And why is this transaction happening?

If they still think something is wrong, they report it to the right authorities, like the Financial Intelligence Unit (FIU).

2. Real-Time vs. Post-Transaction Monitoring

- Real-Time Monitoring: This system checks transactions as they happen, allowing businesses to immediately block or flag any risky activity.

- Post-Transaction Monitoring: Post-transaction monitoring rules take a step back and look at completed transactions, searching for patterns that might suggest suspicious behavior.

Both types of monitoring complement each other and give a full view of financial transactions, helping institutions catch anything that might slip through.

3. Risk-Based vs Rule-Based

- Risk-Based Approach with AI and Machine Learning: The effective feature of AI-based transaction monitoring systems is that they learn from previous patterns to increase occurrence and decrease false alarms.

- Rule-Based Systems: These systems trigger alerts based on pre-set rules, like a limit on how much money can be transferred.

The Risk-Based Approach with AI and Machine Learning is more advanced and effective in preventing and detecting money laundering activities.

Best Practices in AML Transaction Monitoring in the UAE

The UAE encourages institutions to adopt a risk-based approach to AML, focusing resources on high-risk transactions and customers, such as Politically Exposed Persons (PEPs) or clients from high-risk countries.

Institutions are required to carry out thorough Customer Due Diligence (CDD) and Enhanced Due Diligence (EDD) for high-risk customers. This includes verifying identities, understanding the source of funds, and keeping detailed records for at least five years.

The UAE government places high importance on working closely with international bodies, such as FATF, and regional bodies like MENAFATF. Financial institutions are also required to report any suspicious transactions through the goAML portal in a timely and accurate manner. Here are the top practices:

- Stay Updated on AML & Transaction Monitoring UAE and Global Rules

- Create Clear Transaction Monitoring Rules

- Avoid One-Size-Fits-All Scenarios at All Costs

- Focus on Quality, Not Just Speed

- Always Keep Records

- Use Artificial Intelligence (AI) Transaction Monitoring systems

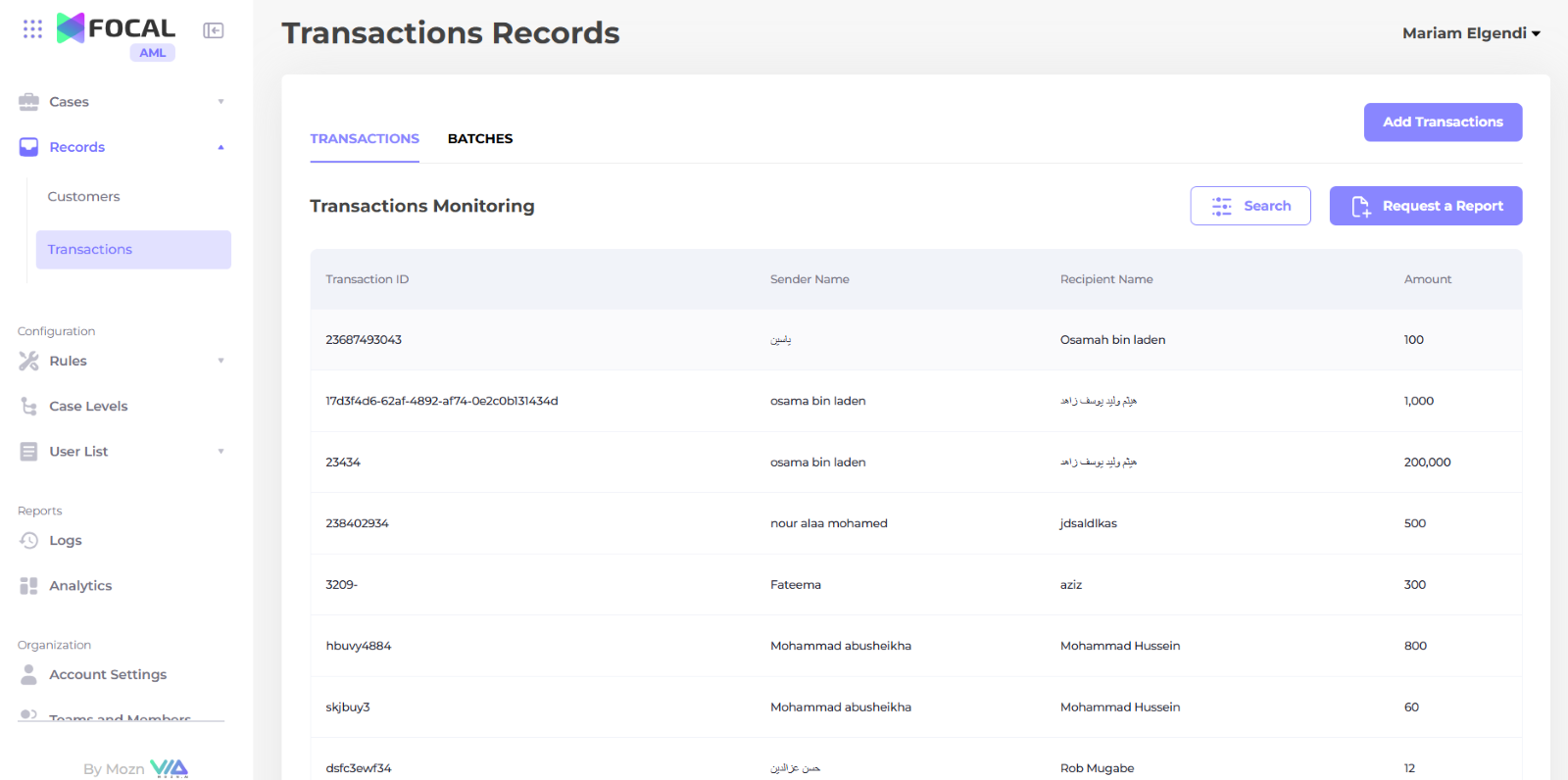

Monitor Transactions in the UAE with FOCAL

The FOCAL transaction monitoring tool enables financial institutions in the UAE to detect suspicious activities such as money laundering, fraud, and internal fraud by analyzing transaction behavior, identifying round-robin patterns which is one of the transaction monitoring examples, and integrating real-time fraud detection and AML monitoring tools.

1. Easy Scenario Builder

The Easy Scenario Builder lets you quickly create and adjust rules for tracking transactions. It helps you spot suspicious actions, cut down on false alarms, and make your system more accurate.

2. Custom Transaction Monitoring Rules Library

You can customize your monitoring system using the Custom Rules Library. You can either choose from ready-made rules or set your own to fit your needs. This way, you can better catch any risky activities that match your specific customer profiles.

3. Real-Time Monitoring

With Real-Time Monitoring, you can check transactions right away—under a second. This quick check helps you find problems fast, so you can stop payments to dangerous or high-risk people right when they happen.

A solid transaction monitoring system offers you the right tools: building rules easily, customizing them to your needs, and checking transactions in real time to keep your financial system safe and up to standard.

Last Thought

The UAE has made big progress in fighting financial crimes by launching a new National Strategy for AMLCFT, and Proliferation Financing (CPF) for 2024-2027. This plan comes after the UAE was removed from the FATF Grey List in February 2024, which shows its strong commitment to improving its financial system.

The strategy focuses on 11 key goals and includes new laws and rules. It uses modern technology and aims to work better with other countries to fight money laundering and cybercrime. If you’re looking for the best AML transaction monitoring system in the UAE, we invite you to schedule a one-on-one consultation call with a FOCAL expert.

.jpg)

.jpg)

.jpg)