IBAN Vs. SWIFT Code: What’s the Difference?

Accelerate AML Compliance: Meet Regulatory Demands with 80% Less Setup Time

Do you use an IBAN, SWIFT, or both? Should you use the IBAN for local transfers? But about the SWIFT code? Are there any differences between the two? Is IBAN the same as the SWIFT code? What would the main difference be if you differentiate between IBAN vs SWIFT Code?

If your job involves checking IBAN numbers, this article on IBAN vs SWIFT Code can help you keep transactions accurate. It can also help you spot any weird differences between the SWIFT code and IBAN number, which might mean fraud.

What is a SWIFT Code?

SWIFT stands for Society for Worldwide Interbank Financial Telecommunication. Banks use the SWIFT system to send and receive money or information safely between banks all over the world. So, in simple terms, a SWIFT code is what banks use for international or wire money transfers.

The SWIFT code also acts as a bank's "ID." For example, the SWIFT code for Saudi Investment Bank is different from the one for Al-Rajhi Bank. This "ID" makes sure the money gets to the right bank account.

A SWIFT code has a mix of letters and numbers and is part of Business Identifier Codes (BIC). It’s a secure, simple way to send money between countries.

When Do I Need a SWIFT Code?

A SWIFT code helps a bank process international payments. But keep in mind that when you use a SWIFT code, you’re not actually moving the money yourself, what you're doing is sending a payment order. So, one of the main things a SWIFT code does is share important information and financial data, such as:

- Account status

- Debit and credit amounts

- Details related to the transfer

Another function of SWIFT codes is streamlining the entire payment process so that it happens in no time. But when do you need it?

- International money transfers

- Receiving money from abroad

- Making international payments for goods and services

- Opening an account in a foreign country (mostly for business accounts)

How to Find a SWIFT Code

Usually, you can find your bank's SWIFT code on the bank statement or online banking portal. It can also be on the bank’s website, or you can contact the bank directly, and they can give it to you. It usually consists of 8 to 11 characters, combining letters and numbers that denote the bank, country, location, and branch.

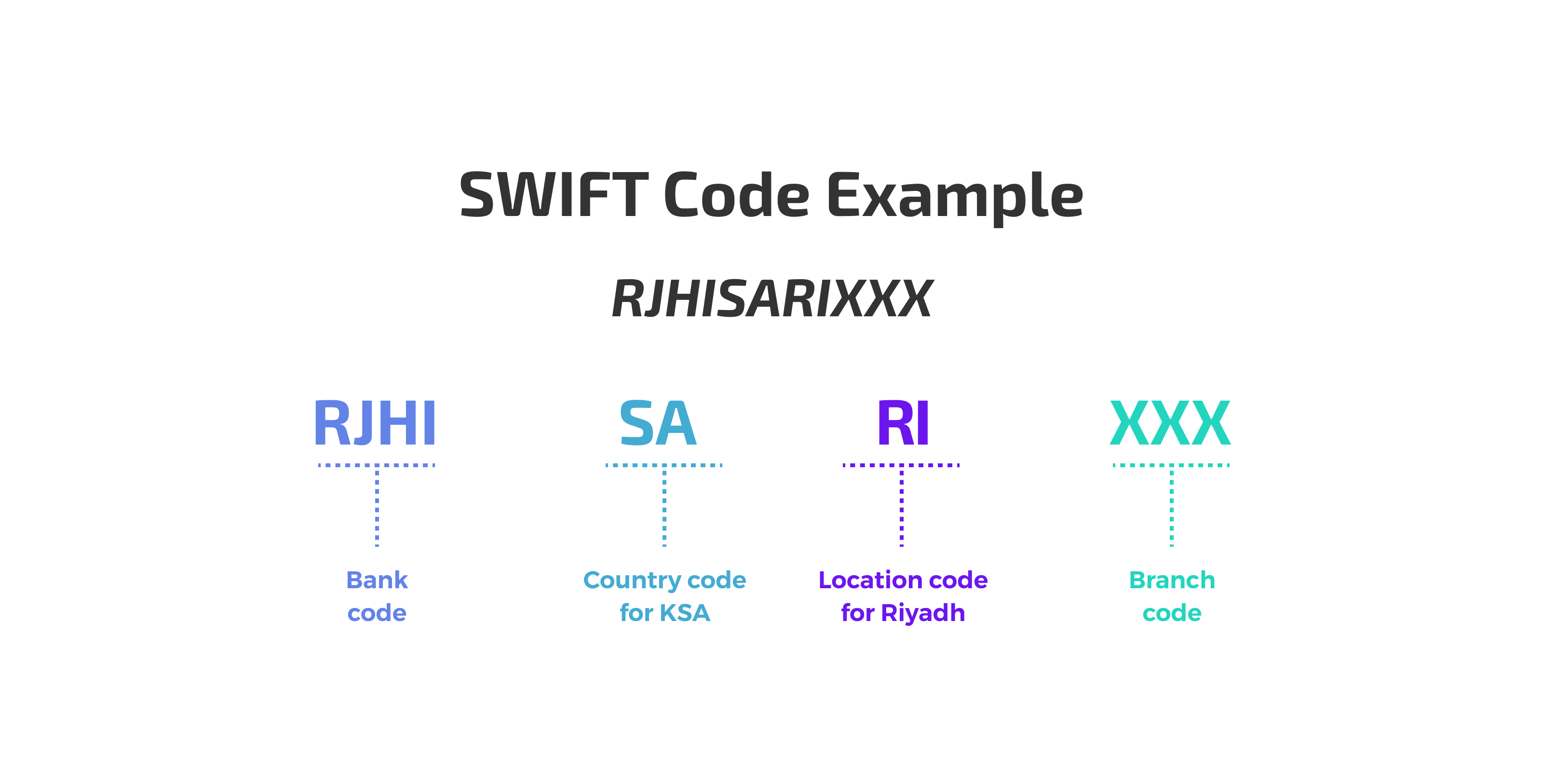

Example of a SWIFT Code

The SWIFT code numbers follow an international standard format for financial transactions, and it might look like this:

RJHISARIXXX (for Al Rajhi Bank, Riyadh, Saudi Arabia).

What does a SWIFT code look like?

Here is a breakdown of the SWIFT Code:

- RJHI: Bank code for Al Rajhi Bank.

- SA: Country code for Saudi Arabia.

- RI: Location code for Riyadh.

- XXX: Optional branch code (indicating the main branch in this case).

Learn more about Anti-Money Laundering Compliance in Saudi Arabia

Is a SWIFT Code The Same as a Routing Number?

No, a SWIFT code is not the same as a routing number. Yes, they’re both used to identify financial institutions, but they serve different purposes and are used in different contexts.

Basically, SWIFT codes are alphanumeric and longer, whereas routing numbers are numeric and shorter. Also, SWIFT codes are for international transactions, while routing numbers are primarily for domestic transactions within certain countries (like the U.S.).

Comply quickly with local/global regulations with 80% less setup time

What is an IBAN Number?

The International Bank Account Number stands for IBAN, which is similar to the SWIFT code and also identifies bank accounts. However, IBAN numbers are only used by specific countries like European countries and some others, but not the United States, for example.

What do you need an IBAN for?

Similar to SWIFT codes, IBAN numbers are also used for:

- Sending money overseas

- Cross-border transactions

- Domestic transactions within the same country

- Online purchases

- International businesses

Structure of an IBAN in GCC Countries

An IBAN in GCC countries typically follows the same structure:

- Country Code: 2 letters (e.g., SA for Saudi Arabia, AE for UAE).

- Check Digits: 2 digits that help validate the IBAN.

- Bank Code and Account Number: Vary depending on the country and bank.

See the following examples:

- A Saudi Arabian IBAN: SA03 8000 0000 6080 1016 XXXX

- A UAE IBAN: AE07 0331 2345 6789 0123 XXX

Learn about Anti-Money Laundering (AML) Laws in the UAE

Do you need an IBAN if you have the SWIFT Code?

It depends. If you’re sending money to a country that uses both the IBAN and SWIFT codes, then it is possible to be asked for both codes, but we established that some countries do not use the IBAN system and hence if you’re sending money to these countries, only a SWIFT code will be required.

IBAN Number Vs. SWIFT Code

Generally speaking, an IBAN number identifies individual accounts within specific banks, but SWIFT codes identify banks globally.

The table below explains in detail the differences – IBAN vs SWIFT Codes.

IBAN Vs SWIFT Code: Comparison Table

Check out the Confirmation of Payee product from the FOCAL Platform

Does Saudi Arabia Use an IBAN or SWIFT Code?

In Saudi Arabia, financial institutions use both IBAN numbers as well as SWIFT codes but for different purposes. So, for example, the IBAN system is used in the kingdom for both local and cross-border bank transfers, but the SWIFT codes are generally used for international transactions only.

IBAN vs. SWIFT Code: Last Thought

As of August 2024, 82 countries and territories use the IBAN system, whereas 200+ countries and territories worldwide use the SWIFT code. As for the IBAN vs SWIFT Code difference, IBANs and SWIFT codes are both key for making international payments, but they serve slightly different purposes.

A SWIFT code helps pinpoint the exact bank and branch where the recipient's account is located. On the other hand, an IBAN is often needed for many international transfers to ensure your money reaches the correct account.

So the bottom line for the question of is IBAN and SWIFT code the same? No, they’re not!

.jpg)

.jpg)

.jpg)