What is Payment Screening: Purpose, Process, and Benefits

Accelerate AML Compliance: Meet Regulatory Demands with 80% Less Setup Time

Online payments and real-time transfers are exploding. But with that growth comes a surge in fraud and money laundering risks. According to the United Nations Office on Drugs and Crime, about 2-5% of the world’s GDP, roughly $800 billion to $2 trillion, is laundered every year. That’s huge.

So, financial institutions and businesses have no choice but to stick to strict anti-money laundering (AML) laws. This is where payment screening steps in.

But here’s the rub: making payment screening both effective and user-friendly? That’s a tough balancing act.

In this article, we’ll unpack what payment screening really means, why it’s so important, the hurdles many face, and how smart tech can make it smoother and sharper.

What Is Payment Screening in Banking and AML Compliance?

When a payment is being sent or received across countries, banks, or even within apps, that payment gets checked against watchlists and risk rules.

The goal?

The main goal of payments screening is to make sure the money isn’t going to a terrorist group, sanctioned country, criminal gang, or anyone on a government or global blacklist.

This step happens before the money is processed. If something looks risky, the payment is paused, flagged, or even rejected.

Why Is Payment Screening Needed?

Real-time payments, mobile wallets, and cross-border wires all create more opportunities for criminals to hide dirty money. That's where payments screening helps stop bad actors before they get their money through the system.

Screening is required by regulations like a) OFAC (U.S. Sanctions), b) FATF (Global AML standards), c) EU Sanctions List, and d) UN Consolidated List.

Banks, payment processors, and fintechs are all under pressure to catch red flags. So they screen every single transaction (no matter how small or big), all names, all countries (from and to), and keywords, against sanctions lists, PEP (Politically Exposed Person) lists, and internal blacklists.

So when people ask, What is payment screening? or What is payment investigation? They are actually asking about checking the who, what, and where of a transaction to make sure it’s clean.

How is payment screening different from other types of compliance checks or controls used in AML and fraud prevention?

Sometimes people confuse payment screening with the KYC screening process, transaction monitoring, or KYC name screening. The role payment screening plays in the broader compliance process is to check each individual payment in real time before the money goes out. Meaning, although they all work together, payment screening is not interchangeable with other processes such as screening in KYC AML, KYC name screening, and/or transaction screening AML

Illustrative Example:

Here is a clarifying example to help make this concept easier to understand!

A customer wants to wire money to a charity overseas. But as the payment goes through the bank’s payments sanctions screening system, the charity’s name matches one on the EU Sanctions List. This leads to the payment to be stopped/frozen, and the compliance team steps in to investigate.

Why does this matter?

Because that “charity” could actually be a front for terrorist financing or weapons smuggling.

Key Takeaway:

Payment screening checks every payment, in real-time, to block risky transactions before they happen.

Payment screening is not the same as KYC screening process, AML screening and monitoring, or KYC name screening, it’s the fast, front-line filter that keeps financial institutions safe and compliant.

Comply quickly with local/global regulations with 80% less setup time

Payment Screening vs. Transaction Monitoring: What's the Real Difference?

These two terms often get mixed up. People regularly ask: “Isn’t payment screening the same as transaction monitoring?” The simple answer: No, not even close. They do very different jobs.

1. Payment Screening

Payment screening checks specific payment details before any money moves. It focuses on:

- Who is sending the money

- Who is receiving it

- Which countries are involved

- Words or codes in the message

- Any matches to sanctions or internal watchlists

If anything looks risky, the payment is either paused or blocked right away. This is often referred to as payment sanctions screening, and it's fast, automatic, and essential for preventing illegal transactions before they even begin.

2. Transaction Monitoring

Transaction monitoring looks at patterns and behavior after the transaction has happened. It asks:

- Is someone sending more money than usual?

- Are there signs of money laundering?

- Are payments being broken up to avoid detection?

While payment screening stops known threats, transaction monitoring identifies strange or suspicious behavior over time. It’s what most systems mean when they refer to payment transaction monitoring or AML screening and monitoring.

Why Both Matter

Both tools are required for full compliance with global regulations, but they do different things:

- Payment screening focuses on individual payment risks.

- Transaction monitoring focuses on behavior and long-term trends.

These tools work side-by-side in modern payment monitoring systems and help meet global AML screening requirements.

Key Takeaway:

Payment screening and transaction monitoring are not the same thing.

Screening is the fast check done at the moment a payment is made. Monitoring is the longer-term analysis of account behavior. Both are vital in catching money laundering and fraud.

Why Payment Screening Is Essential for AML and Fraud Risk Management

Every day, banks and payment companies move money around the world and that happens so fast. But that speed comes with risk. It opens the door and the possibility for money laundering, sanctions violations, fraud, and cybercrime. The good thing is that payment screening helps catch these threats before the payment goes through.

So, why is payment screening AML so important?

1. Real-time defense

- Unlike transaction monitoring, which looks at behavior over time, payment screening checks each transaction as it happens.

- It flags anything risky, that is, names, countries, keywords, and either stops the transaction or sends it to compliance for review.

2. Keeps you compliant

- Governments around the world (like the U.S., UK, EU, and UN) require firms to follow strict rules.

- Real time screening against sanctions lists and watchlists is not optional.

- If you miss a risky payment, you could face big fines or even lose your license.

3. Protects your brand

- When a bank or payment platform is caught handling illegal money even if it was by accident, it makes headlines.

- Strong screening systems help avoid these risks and protect your reputation.

4. Stops fraud early

- Anti money laundering screening tools also help spot fake names, spoofed companies, and high-risk countries.

- This makes it harder for fraudsters and criminals to get money into or out of the system.

So, if you’re asking: when is AML screening required? The answer is almost always, especially when it comes to cross-border payments or high-risk customers.

Key Takeaway:

Payment screening AML protects your business, your license, and the financial system.

It’s a real-time filter that blocks known risks long before a transaction becomes a problem.

Step-by-step: How the Payment Screening Process Works

The payment screening process might sound complex, but at its core, it’s just about checking every payment before it’s processed.

Here’s how the payment screening process usually works in banks and financial institutions.

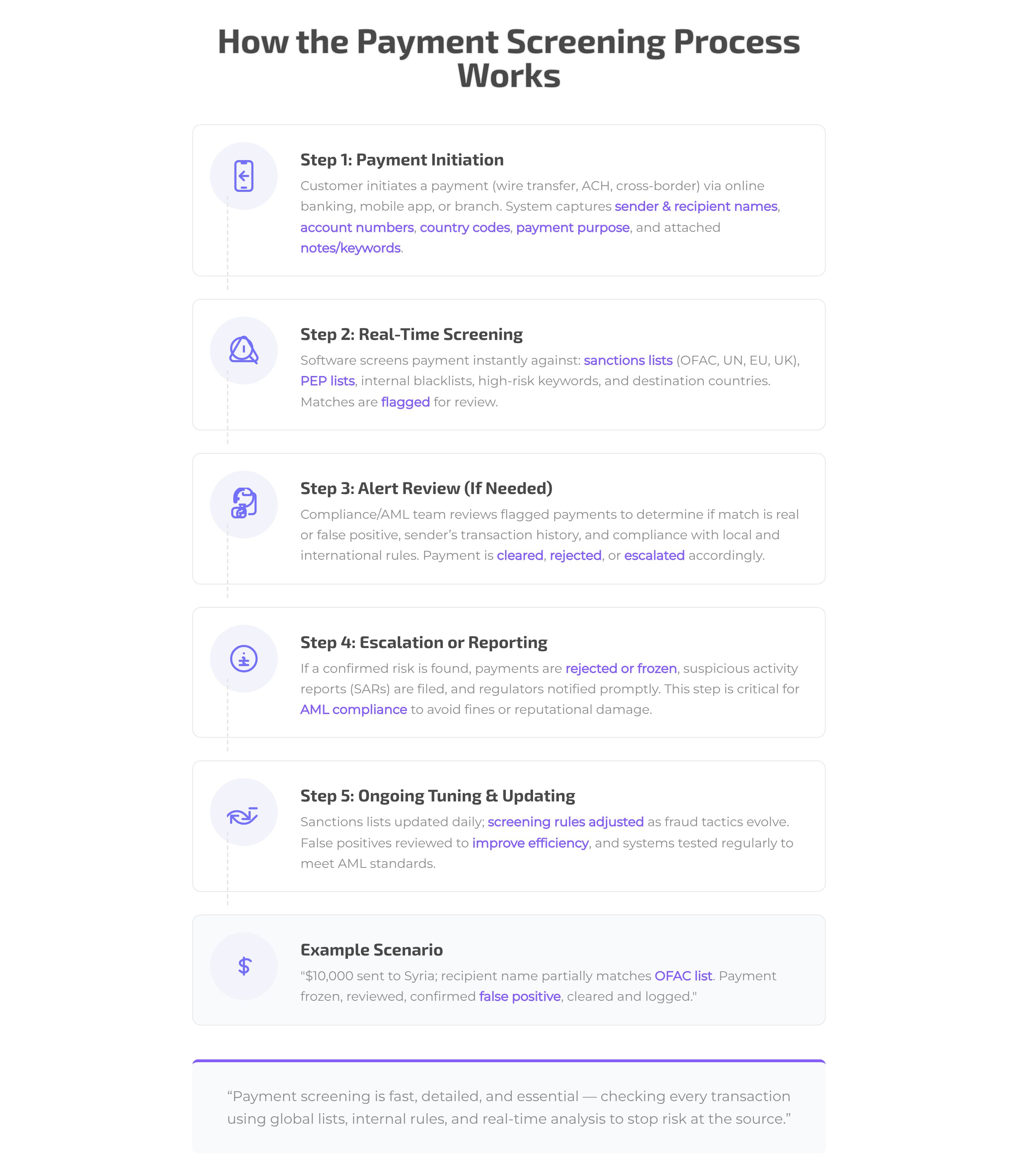

Step 1: Payment Initiation

A customer starts a transaction, maybe a wire transfer, ACH, or cross-border payment. This could happen through online banking, a mobile app, or by visiting a branch.

At this point, the system captures all the key details:

- Name of sender and recipient

- Account numbers

- Country codes

- Purpose of the payment

- Any attached notes or keywords

Step 2: Real-Time Screening

Before the payment moves, real time payments sanctions screening software kicks in instantly to compare the data to:

- Sanctions lists (like OFAC, UN, EU, UK, etc.)

- PEP lists (Politically Exposed Persons)

- Internal blacklists

- High-risk keywords and destination countries

If the system sees a match, even a partial one, the payment is flagged for review.

Step 3: Alert Review (If Needed)

If a transaction is flagged, the compliance or AML team steps in to check:

- Is the match real or a false positive?

- Does the sender have a history of clean transactions?

- Is the payment allowed under local and international rules?

Depending on the findings, the payment is either cleared, rejected, or escalated.

Step 4: Escalation or Reporting (If Risky)

After the payment investigation process, if there’s a confirmed hit, for example, the payment is going to a sanctioned entity or person, the institution may:

- Reject or freeze the transaction

- File a Suspicious Activity Report (SAR) or equivalent

- Notify regulators immediately

This is a critical part of screening in AML compliance, especially in regulated markets where failure to act can lead to fines or reputational damage.

Step 5: Ongoing Tuning and Updating

A big part of the screening in KYC AML process is maintaining up-to-date data. That means:

- Keeping sanctions lists updated daily

- Adjusting screening rules as fraud tactics evolve

- Reviewing false positives to improve efficiency

Institutions also test their systems regularly to meet AML screening requirements and industry best practices.

Example: How It Works in Practice

Let’s say a customer sends $10,000 to a company in Syria.

The name of the recipient partly matches a person on the OFAC list.

The system freezes the payment and alerts compliance. After review, it turns out to be a false positive — the names are close but not the same.

The payment is cleared, and the system logs the decision for audit purposes.

Key Takeaway:

The payment screening process is fast, detailed, and essential.

It checks every transaction before it moves — using global lists, internal rules, and real-time analysis to stop risk at the source.

Key Regulations That Drive Payment Screening

Regulations across the globe make it clear: If you're moving money, you need to screen it.

Let’s walk through the key rules and global standards that shape how the payment screening process works and what makes it legally required.

1. FATF Recommendations (Global AML Framework)

The Financial Action Task Force (FATF) sets the tone for AML worldwide. While it doesn’t enforce laws directly, its recommendations are the global standard.

FATF says institutions must:

- Identify and report suspicious transactions

- Screen against sanctions lists

- Use risk-based controls for high-risk payments and customers

This forms the backbone of AML screening and monitoring obligations in most countries.

2. OFAC Sanctions (United States)

In the U.S., banks must follow OFAC (the Office of Foreign Assets Control). OFAC maintains a list of 1) Sanctioned individuals, 2) Companies, 3) Countries, and 4) Vessels. If a payment matches any of these, it must be frozen immediately.

This is where payment sanctions screening becomes critical and why real time screening is a must-have in every system, It is simple: Missing a match? That’s a serious violation and penalties can reach into the millions.

3. European AML Directives (EU)

The EU has several AML laws, each one strengthens a different part of AML compliance like Customer due diligence, Screening in KYC AML, Reporting requirements, Sanctions enforcement, and more.

Firms in Europe are expected to combine KYC name screening, payment screening AML, and ongoing transaction screening AML as part of a risk-based program.

4. UK Sanctions and AML Laws

Post-Brexit, the UK enforces its own sanctions regime via the Office of Financial Sanctions Implementation (OFSI).

Banks and payment providers must screen all outbound and inbound payments against UK-specific lists, as well as perform:

- Payments monitoring

- KYC screening process

- AML screening requirements based on domestic law

Failing to screen properly here can lead to license restrictions or public enforcement notices.

5. APAC and Other Jurisdictions

Countries like Singapore, Australia, and the UAE have strict AML regimes as well. Most follow FATF’s core recommendations and add local enforcement layers.

Screening in these countries must align with:

- Local regulator requirements

- FATF compliance expectations

- Country-specific sanctions programs

This global landscape means you must build a payment monitoring system that adapts fast and works across multiple jurisdictions.

Read more: Sanction Screening in the UAE: What to Do if a Customer is Listed

Key Takeaway:

Payment screening is required by law in almost every jurisdiction. Whether it’s OFAC, FATF, or EU directives, regulators expect every single transaction to be checked before it’s processed, and failing to do that can lead to serious penalties.

Common Challenges and Risks in Payment Screening

Payment screening is essential but far from perfect. Even advanced systems face issues that can lead to missed threats or unnecessary alerts.

1. Too Many False Positives: Overly sensitive screening rules flag legitimate transactions, overwhelming teams and delaying reviews.

2. False Negatives and Missed Risks: Weak or outdated screening in AML setups can let suspicious payments pass through unnoticed.

3. Outdated Sanctions and Watchlists: Without real-time updates, your payment sanctions screening system may miss newly sanctioned entities.

4. Incomplete or Poor Data: Missing or incorrect fields (names, countries, etc.) reduce accuracy in AML KYC screening and cause faulty matches.

5. Regulatory Variations by Region: A payment may be fine in one country but blocked in another. Transaction screening vs transaction monitoring rules often vary by region, requiring smart systems that adapt fast.

6. Heavy Manual Workload: Too many alerts slow down operations and stretch compliance teams, especially when real-time screening is required.

Top Payment Screening Best Practices for AML Compliance

Stronger payment screening starts with smarter action.

- Use Real-Time Screening Tools and AML KYC Screening Solutions

- Update Sanctions & Watchlists Daily

- Configure Risk-Based Rules

- Automate Escalations for High-Risk Payments

- Clean and Enrich Your Payment Data

- Train Staff on Screening Red Flags

- Integrate Screening Across All Channels

- Test and Audit Screening Performance Regularly

- Leverage Analytics and Dashboards

- Align Screening with Broader AML Programs

A Unified Platform for Financial Crime Prevention and AML Compliance

If you want to strengthen your AML screening process, you need more than just a basic tool, you need a solution that understands real-world AML challenges.

FOCAL is an all-in-one financial crime prevention platform designed for banks and financial institutions. It helps tackle a range of challenges like AML compliance, transaction monitoring, customer due diligence, and fraud prevention, all from one place.

By combining these key functions, FOCAL makes it easier for compliance teams to spot suspicious activities quickly and accurately. It supports real-time screening and risk assessments, ensuring that institutions can act fast and meet regulatory requirements without the usual hassle. With FOCAL, financial institutions get a flexible, powerful platform that simplifies complex workflows and strengthens defenses against financial crime.

.jpg)

.jpg)

.jpg)